So, what happens if we combine the two factors…?

The aim here is to show the impact of fees together with the investment portfolio you are invested in and how these two factors combine to give you either a poor or great outcome at retirement.

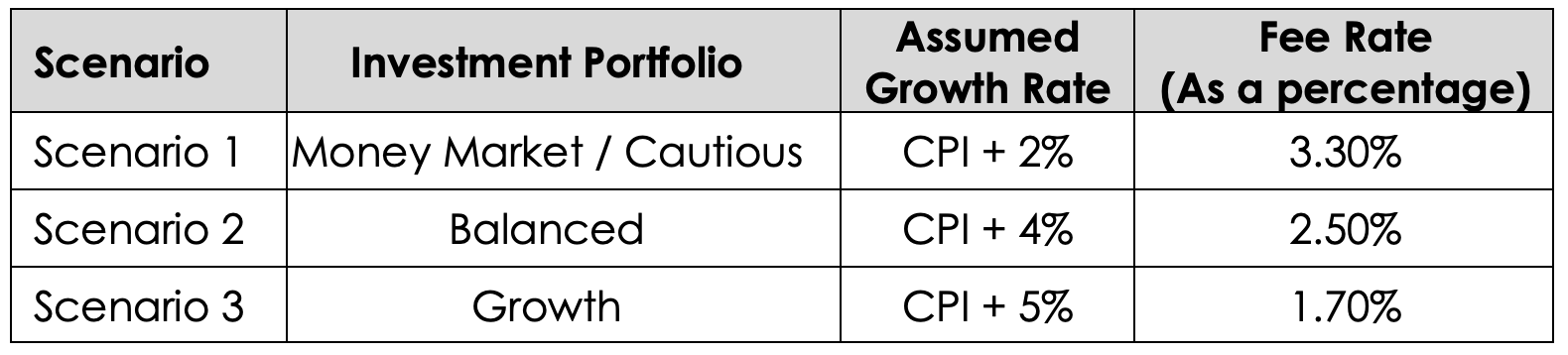

Let’s take Mr X again, however, for the last discussion, we have the following three scenarios:

Based on the above factors, the outcome is illustrated below:

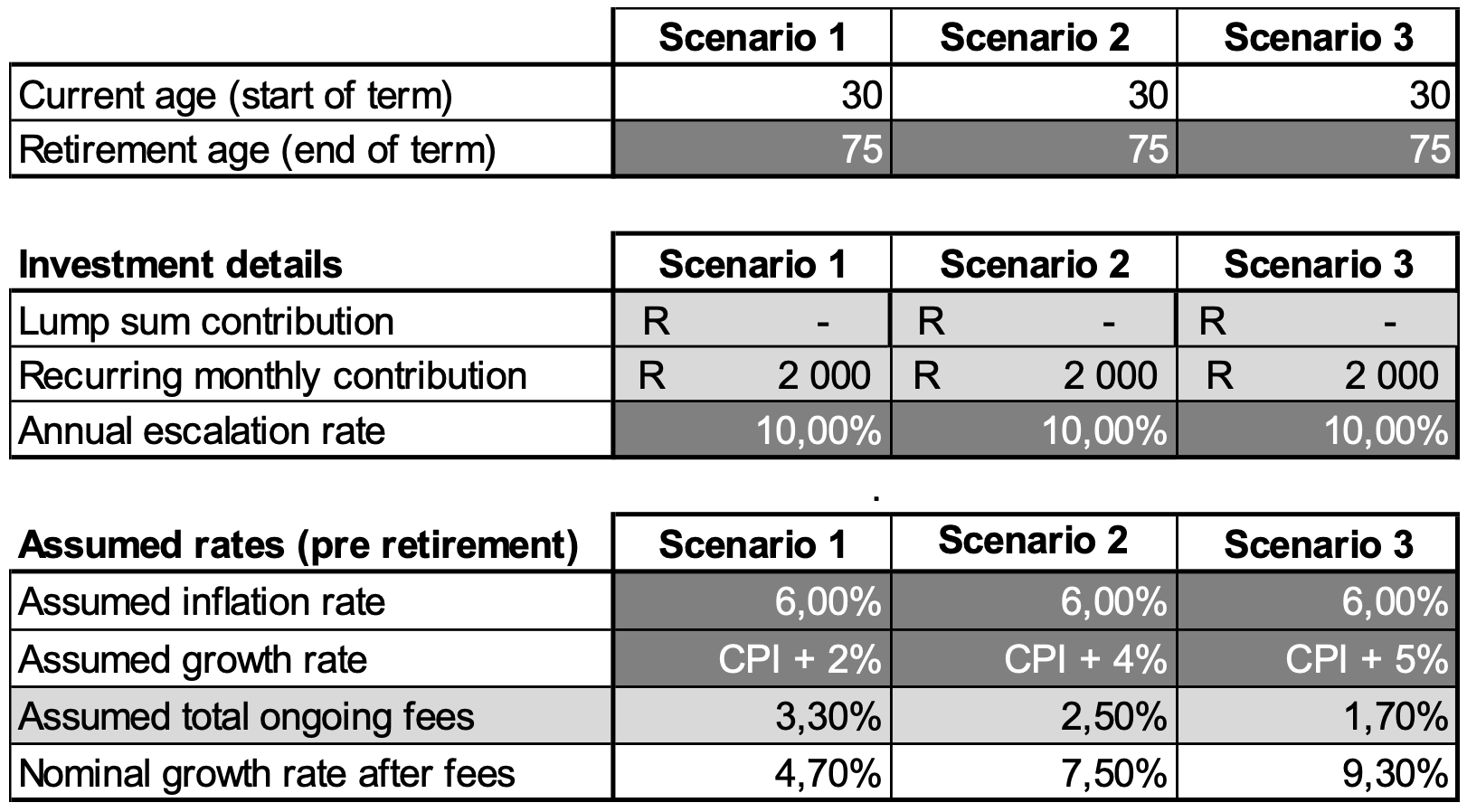

Using the above information, the impact is illustrated below:

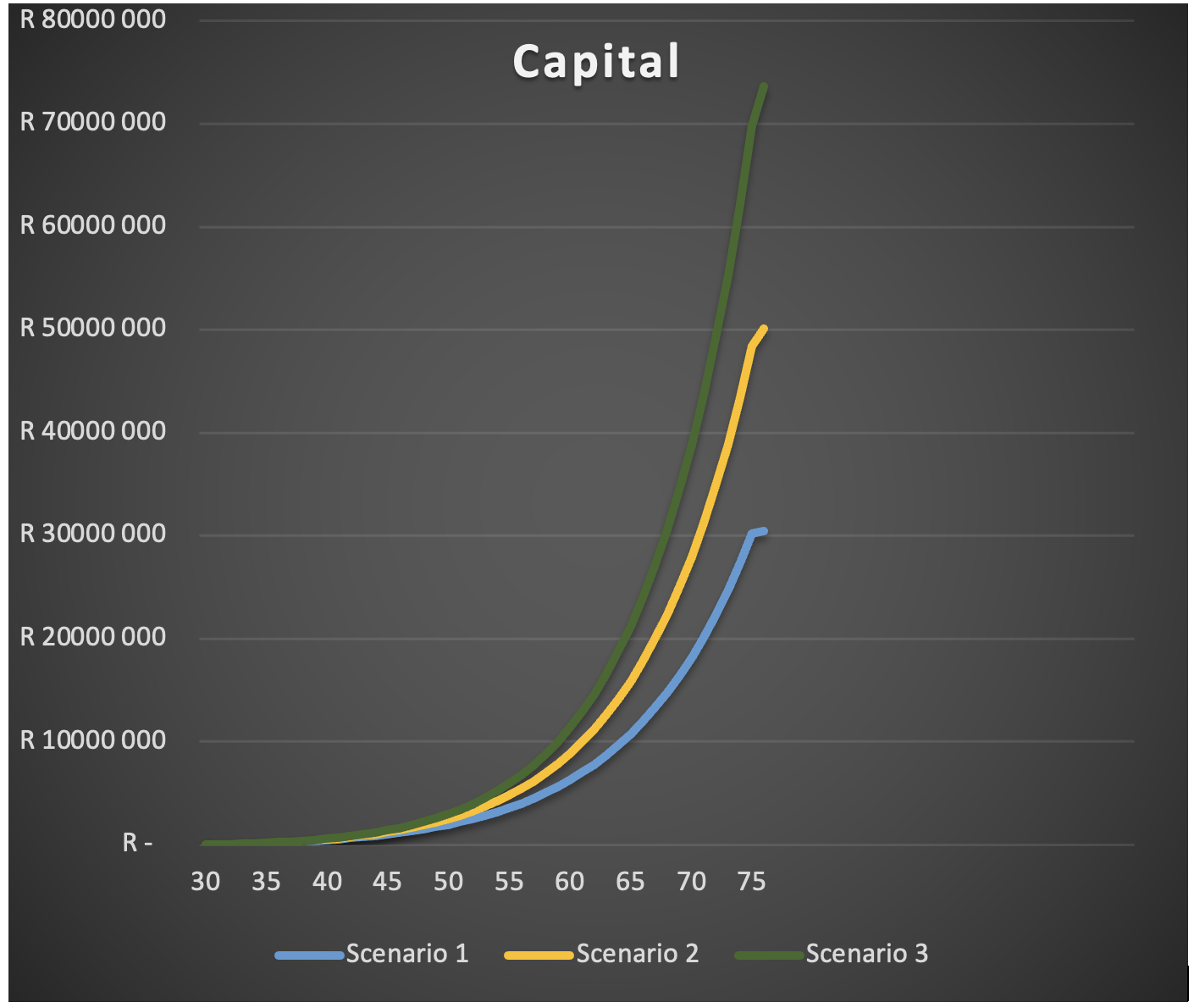

How does that outcome look on a graph? Here it is…

The differences are very notable, as shown in the graph above and in terms of the figures presented below. Therefore, if you compare high fees, together with an incorrect investment strategy, versus a correct investment strategy with low fees, the difference is astounding, further shown in the values below:

- In terms of your capital value at retirement (age 70) the difference works out to around R39 million,

- As a present value converted back from the future value, in today’s terms, at 6% inflation, the difference is R2.6 million.

What you end up seeing is that by pairing lower fees with the correct investment strategy, and understanding that strategy, and your end destination (retirement goal), provides you with a better outcome at retirement.

It all starts with understanding how you want to spend your retirement and the retirement journey. So, are you going to stop working, are you still going to enjoy doing work or a hobby that pays you a monthly income, extending your investment time-horizon? What’s your poison? Or do you totally need to think outside the box for your retirement?

Wherever your retirement journey takes you, always remember that you will need assets in your old age to provide you with a solution at retirement… ensuring you have an income at old age. Trust us, you don’t want to miss this one…

During your retirement journey, remember to consistently check how fees impact your retirement investments, and ensure that you have an investment strategy in place, you stick to that strategy, and make changes when needed with your registered independent financial advisor – remember things change, you need to be adapt.

Lastly, together with the BankerX crew, we have started sourcing different quotations from different providers in the market. It’s important to understand that the costs reflected on the website of service providers and their fund fact sheets aren’t the costs always quoted. The proof is in the pudding!

Keep your eyes peeled for the comparison between different providers in the market, where we compare costs on the different platforms (LISP versus LIFE), based on the providers’ default Regulation 28 investment portfolio (passive/index strategies), focusing on retirement annuities in the market.

As an added bonus, in the next article we will also explain why you should consider taking the termination/penalty fee to move your retirement investment to a more competitive provider, in terms of fees and the outcome at retirement.

Happy retirement!