If you haven’t read the previous blog on investment strategy, please click here to read it now.

In this blog, we tackle the fees of a retirement annuity and what impact they have on your retirement journey.

Let’s use Mr X as an example, to understand the impact of fees, then the impact of the investment strategy, and then a combination of the two.

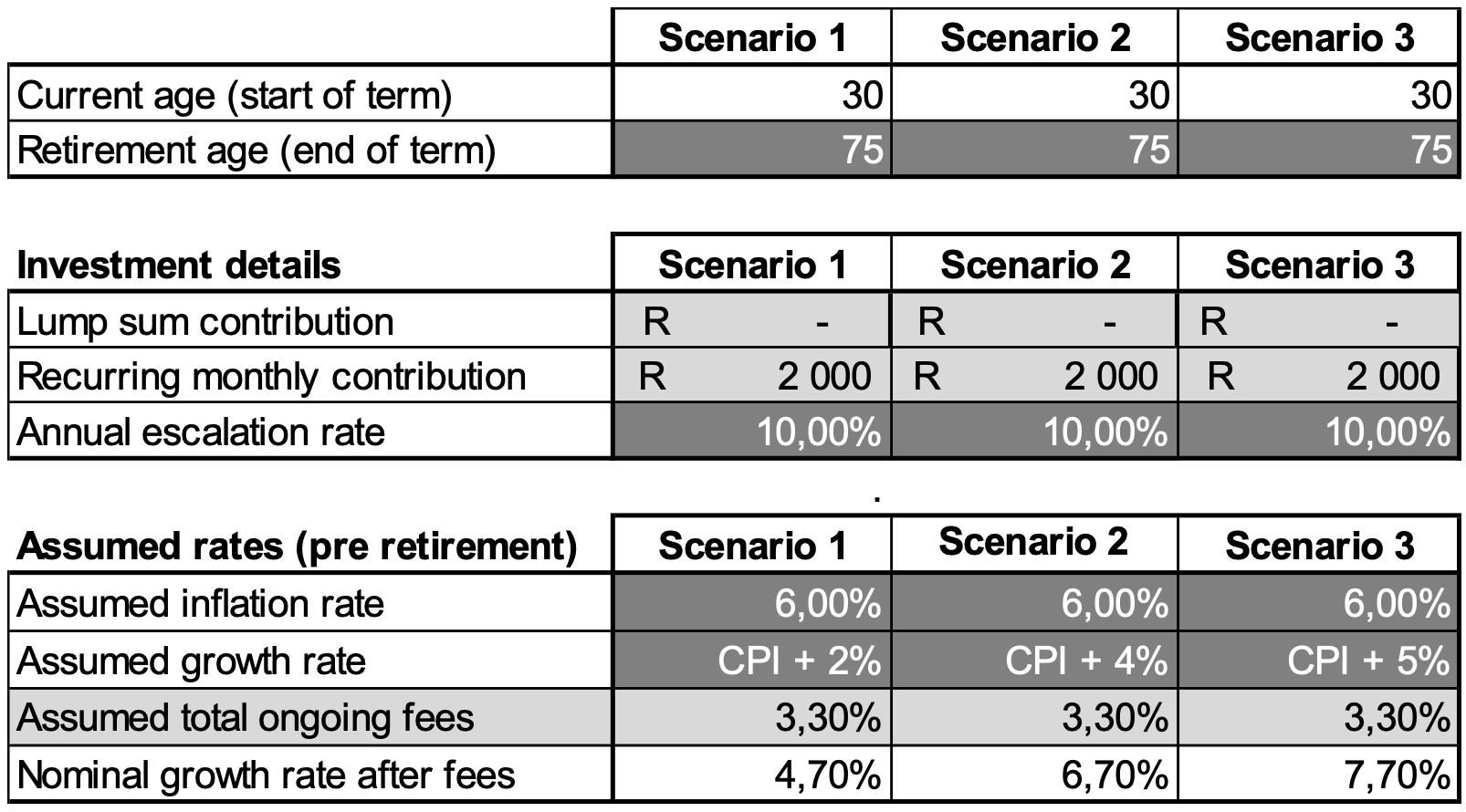

In the first example, Mr X has the following factors influencing his investment strategy in terms of the retirement journey:

- Mr X starts contributing towards retirement from age 30 (monthly). He is looking to access the capital amount, for retirement purposes, at age 70 – so effectively 40 years to invest is his timeline.

- Mr X starts contributing at R2000 per month, and the contribution amount escalates at 10% per annum, before costs.

- In the calculation we assume an inflation rate of 6%, a tad high versus what inflation currently is, however, we like to err on the side of caution, therefore we use the higher inflation rate of 6%.

- We further assume that the member is in the correct investment portfolio, which is growing at CPI (Consumer Price Index, or better known as inflation) plus 5% – based on growing his retirement monies.

We then assume three (3) different fee rates (which is payable monthly, and illustrated below):

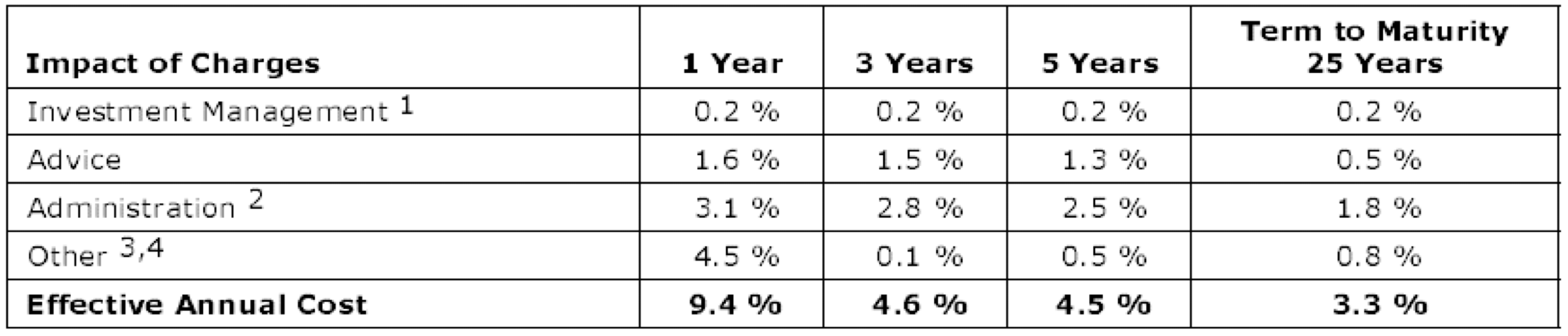

The fees illustrated above are the total effective annual cost, better known as EAC in the industry. This EAC is broken down below into their different components:

Below is an explanation of the different charges, in this case, the Fund was a Liberty (insurance provider) investment portfolio. The important part is to understand what additional fees you are paying, and how those fees could impact your retirement results. Please refer to note 3 + 4 in terms of other above:

Based on the factors above, below is an extract of Mr X’s calculation we use to understand the impact of fees on his long-term investment strategy (a basic breakdown):

You will note that the only difference here is the fee being charged per scenario and everything else remains exactly the same.

Here are the results of the different fees being compared, based on capital at retirement versus the present value (PV) in today’s terms:

You can see where the fees are manageable and low (scenario 3), the retirement outcome at age 70 is substantially better, than where the fees are high and become unmanageable (scenario 1).

Example number two, what happens if Mr X was charged the same fee, however the investment portfolio they invested in was a cash (money market) or cautious (low equity) type portfolio for the same 40 years?

How does that stack up against a high growth and balanced portfolio? Results below:

Above you will note that the fee used was the higher fee, being 3.30%. The only change here is that Mr X was put in the following types of investment portfolios, based on his investment strategy:

The outcome is:

As the scenario indicates, the lower the assumed growth rate, the less your retirement outcome will be in 40 years, with everything else being the same (scenario 1). A portfolio providing more growth (which comes with volatility) has a better outcome when held as a long-term investment (scenario 3). Strap in for a bumpy ride.

It is important to remember that selecting the incorrect investment portfolio is as detrimental to your retirement goals, as high fees.

You need to make sure you understand why you are investing, what your goal is, and invest to reach it, and here liquidity becomes key in your financial plan. Speak to a registered independent financial advisor when looking into that financial plan.

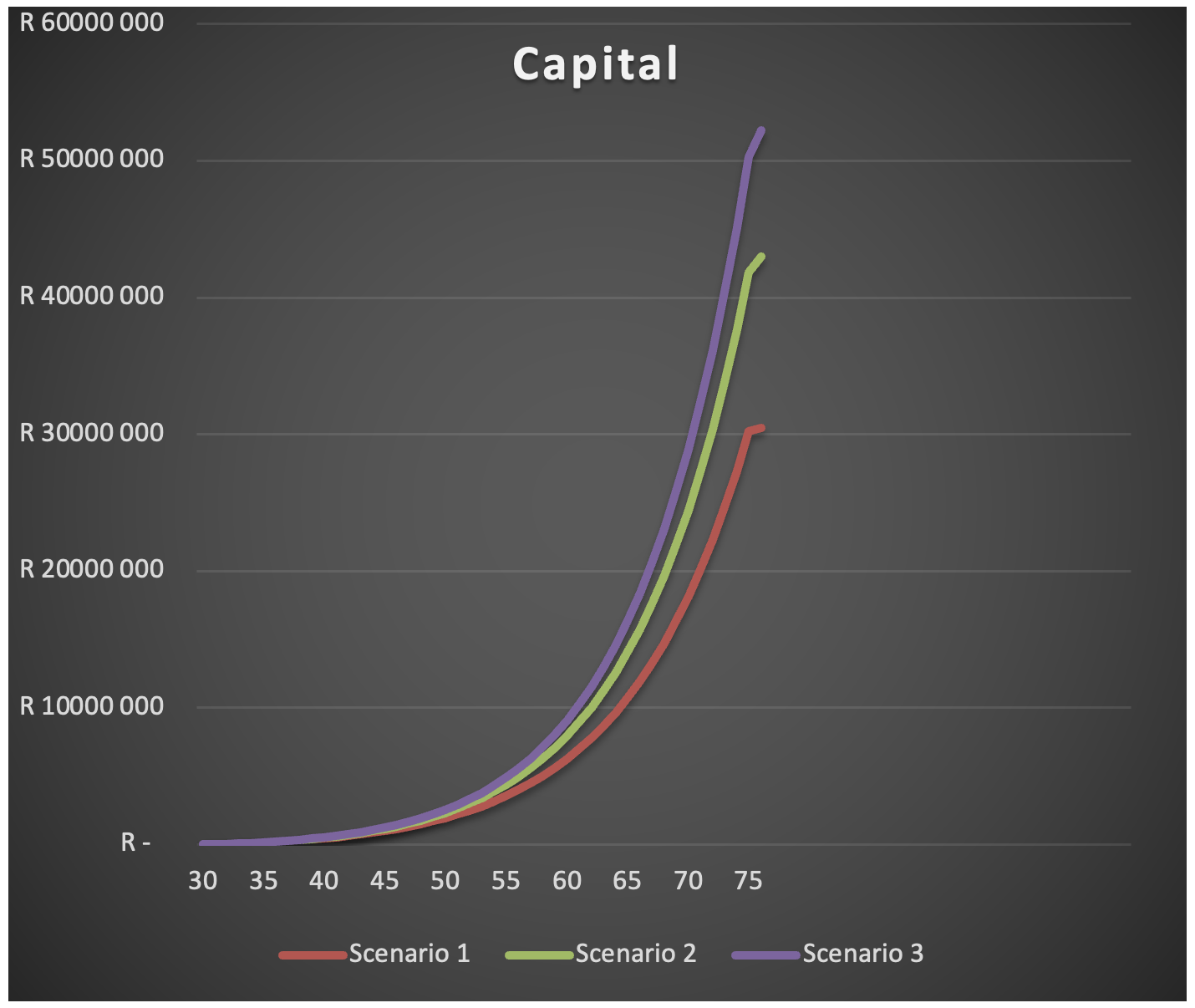

Below is a graph showing the impact of the different growth rates of the different investment portfolios, on your retirement outcome.

The graph clearly indicates that a CPI + 2% investment strategy (scenario 1) doesn’t come close to the retirement outcome of the CPI + 5% investment strategy (scenario 3).

Again, understand volatility, and how markets move, and that you need to adopt an investment strategy for the long term and stick to it.

If you don’t like it or can’t stomach it, make sure you speak to a registered independent financial advisor to help.